The pricing model used by retailers varies wildly when it comes to how much money they take up front. Consultant Toby Griffin weighs up the arguments…

Every purchase has risk attached for both the seller and the buyer. The saying ‘you pays your money, you takes your choice’ suggests a norm where money is handed over before the goods are taken or ordered. These two issues – risk and timing – are the backbone of our decision-making process when setting the structure of a business’s payment terms.

Having worked in six different businesses within the KBB industry, I have seen all manner of payment terms, from one extreme to the other, with everything from payment on account (ie no deposit or interim payments); 25% deposit and balance on completion; 45% deposit, 45% on delivery, and 10% on completion; to 80% on order and 100% on order.

All of the businesses concerned are successful and have happy

cus–tomers, good financials, and are growing, so I can safely say that there is no correct answer here.

So how and why do so many businesses within our industry vary so wildly on what is a pretty important subject? Ask your finance director if you think that it isn’t!

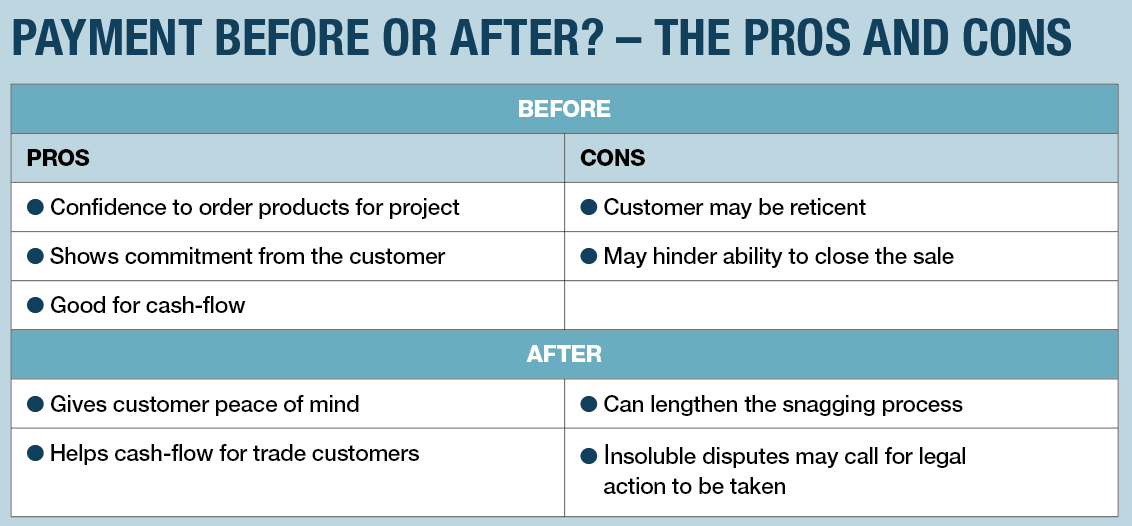

Let’s first look at the arguments for ‘front-loading’ payments, where you take most or all of the money at the point of order.

Turnover is vanity, profit is sanity and cash is reality. Having the money in your bank rather than your customers’ is generally a very good idea. And so, from a pure cash-flow perspective, front-loading of client

pay–ments means you are safe to order the products – particularly if on pro forma – and take delivery, knowing that the money will be there to pay for them, even if the installation or completion of the project is delayed.

Of course, unless your paperwork clearly states that deposits are non-refundable, a customer has sound legal grounds to request the return of a deposit. In all of my years, however, I have only once had to give back a customer’s deposit.

Taking a large chunk of money upfront shows total commitment on behalf of the customer, and pretty much guarantees that the project is going ahead. You can book in installers, order products, and rejoice at another sale, confident that this is a ‘goer’.

Power is another important factor. Up until the point the first money is handed over, the power is entirely with the customer. When money changes hands, the power dynamic changes too. The relationship is then a legal one and, in the eyes of the law, both parties are on an equal footing, and, apart from certain consumer protection rights, the retailer can avoid having to make expensive, awkward compromises or commitments in order to please the customer from then on. I’m not saying that the retailer should not be accommodating and customer-focused, but it then becomes a choice to do so.

So although sometimes an awkward conversation, is it really a problem to ask for a big financial commitment upfront? As Barry Collins, MD of Schwarz Kitchens in Eastbourne, once told me:

“Cus–tomers have decided who they are going to buy from before they get to the point of finding out payment terms. They have usually committed hours of one-to-one time with their chosen designer by the point they decide to go ahead. It’s genuinely not that big of a deal to just ask for all of the money at that point.”

So if a customer asks why so much is required at that stage, what do you tell them?

You could start by explaining that products need to be ordered and payment could be due immediately; a lot of work has already been done for free – measure-up/site survey, design, specification, presentation; fitters need to be booked, and deliveries allocated. To reverse all of this if the customer changes their mind is expensive and time-consuming.

So what then are the arguments against taking the payment upfront?

The big one here is about trust. Having heard horror stories of companies going bust and rogue traders, many customers can be worried that they are about to give you a lot of money, when it could be many months before they have anything to show for it. This fear, despite your calm reassurances, undoubt-edly makes closing the sale more difficult in some cases, and can be a deal-breaker in others.

I have found that offering some sort of compromise at this point can normally keep the deal afloat, and explaining the benefits of paying the deposit by credit card can really help too, although the card fees make this a less preferable option.

Another small problem with front-loading payments is strangely the overly positive cash-flow image that it gives. Although we all do some kind of cash-flow forecasting, it can be tempting to just look at the bank balance on a given day, lick your lips, then spend the money on something that was not completely necessary. It’s human nature, and not that easy to resist.

On the flip-side, what are the arguments for taking payment after delivery?

There is no doubt that leaving large balances outstanding gives the customer peace of mind that you are going to deliver the project and will also help sales. How much of a difference this makes depends on the trust that the customer has in you and your business, but it certainly makes some difference.

In the case of account customers, for example tradespeople who might be buying multiple kitchens and bathrooms from you a month, loading all of the orders into one monthly statement can help to keep down the admin and, by aiding their cash-flow, they will be more inclined to order from you.

But what are the pitfalls of waiting for your payment?

Well, as Ian Palmer, a designer at Umbermaster Kitchens in Kent, warns, snagging lists can become a real and never-ending problem with balances outstanding.

“It’s interesting that even with an amount retained, some still want more,” he says. “It becomes the same conversation about trust and, yes, when a client is really attached to holding money back, you know they probably have a plan.”

I know from personal experience that, on average, the greater the balance outstanding, the longer the snagging lists. Not only that, new lists have a habit of appearing just when the last list is nearing completion. Trying to judge whether the client is just very particular, or in fact gearing up for some kind of discount, is an art. Being willing to take legal action can really help if discussions start to sour. A balance of less than £10,000 can be addressed cheaply and easily in the small claims court, without legal representation.

I hope I have covered most of the arguments for and against a chosen payment structure, and there are, of course, a lot of other options and considerations. For example, finance, deposit protection schemes, custo-mers paying installers directly etc, but these are for another day.

So let’s conclude by coming back to the two issues of risk and timing. Do you trust your customer to pay at the end of the job? Do they trust you to deliver as expected? Do you need the cash-flow? Do they have the money now?

Payment in advance is good from an operational and financial sense, payment on completion is good for sales. As business bosses, you must decide which is right for you.

You pays your money, you takes your choice.