The kbbreview retailer survey 2026

Every two years, as we build up to kbb Birmingham, we take an exclusive snapshot of the UK independent kitchen and bathroom retail sector in the kbbreview Retailer Survey. Trading conditions, business confidence, cashflow and profitability are all examined as we take a look at what it really means to be a retailer in 2026…

Much has been said about the overall state of the industry in the last 12 months, but as the results of this year’s survey reveal, despite the doom and gloom, roughly a third of all UK KBB retailers said their trading conditions had been better – or even much better – over the last 12 months.

A total of 31% retailers said they’d seen positive trading conditions throughout 2025, but just over a quarter (26%) said it was worse or much worse. Trading conditions seem to be slightly better for those who sell solely or mostly bathrooms compared to their kitchen equivalent – 37% said better or much better compared to 29% for kitchens. Equally, 15% said conditions were worse or much worse in bathrooms against 29% of kitchen retailers.

The reasons for improved trading were a mix of leaning into recommendations and heritage as well as upping marketing activity.

“There has been an improvement in buyer confidence,” one retailer said, adding that they’d seen an increase in “homeowners deciding to stay where they are and improve their property, such as adding more bathrooms”.

Another recalled: “I had planned for a year similar to 2024 but we have done slightly better – clients seem to have slightly higher budgets. Given how tough things are globally and with the economy it’s a nice feeling to have improved on last year.”

And looking ahead, nearly a half (48%) of all retailers said they were confident about their business performance in the next year and, in fact, 15% more said they were “very confident”. 15% still said they weren’t confident, however. This was very similar for both kitchens and bathrooms.

When asked why they were more optimistic this year than last, most retailers had the same answer. “There’s pent-up demand,” one kitchen dealer summed up. “Our order book and pipeline of work is much higher than this time last year”.

And for many of our retailer respondents, that’s not just blind optimism either, because they’ve entered this year with full order diaries several months in advance, which is a marked improvement of where they were a year ago. Several retailers encouragingly said their teams are booked until April, a few until at least May, and some very busy retailers reported having at least the first six months of the year fully booked out already.

Although thankfully only a small minority, retailers who weren’t confident about the rest of the year blamed a range of factors, including the general cost of living, as well as inflation, higher interest rates and lack of confidence.

“Uncertainty’s still hanging around,” thought one kitchen retailer. “The budget’s not helped at all either. We need the property market to move quicker, particularly for planning applications!”

Industry confidence

What is interesting is that while most retailers are confident about themselves in 2026, they are not as confident about the wider KBB retail market, with 32% saying they were confident or very confident – compared to 63% about their own business.

Bathroom retailers were more pessimistic about the wider market with 29% saying they weren’t confident compared to 14% for kitchens.

One retailer, who predominantly sells bathrooms, said: “People of all ages are feeling the strain, whether it’s on their jobs, their return on investments, or just the cost of everyday items.

We are all under strain and the first things to go are the big ticket items that can be left a year or two like a new bathroom or kitchen. Instead, they’re spending it on enjoying themselves to give themselves a little pleasure, like meals out, days away, or holidays.”

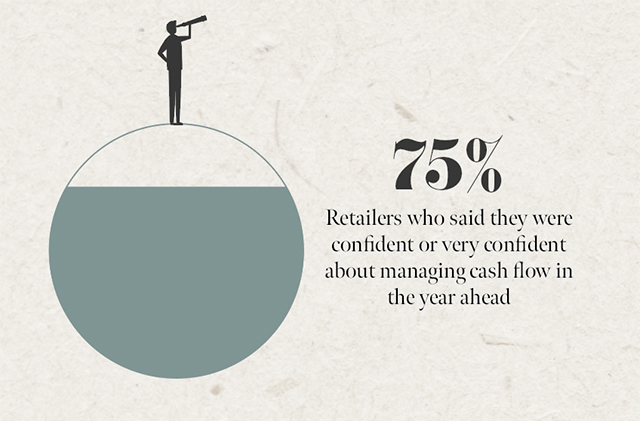

Despite this mixed view of confidence in the market, three-quarters of retailers said they were either confident or very confident about managing cash flow with just 4% saying they were unconfident – the rest said it was just average.

Equally, there’s very little doom and gloom when it comes to profits – nearly one in five (37%) said they were expecting profitability to increase and another 46% saying it would stay the same.

Again, lots of retailers pointed to their growing order books as a prediction of good things to come this year. Still, lots of retailers also say they’ve been proactive and made both big and small changes to their business, which should hopefully pay dividends in the year to come.

Some retailers said they’d be making a more conscious effort to pursue larger-scale projects, where margins can be made up across multiple rooms in a single property. Meanwhile others have found ways to improve their workflow, efficiencies and productivity over the past year.

“With a new display, we certainly have lots to shout about and it will provide a great marketing tool to build relationships with more architects in the local area,” explained one retailer. “It’s just so hard to predict what’s ahead of us, but positivity is the key to keeping going!”

Orders and enquiries

38% of retailers said enquiries were up and, in fact, 11% said they had increased a lot. A quarter said they’d remained the same but 37% said they’d decreased either a bit or a lot.

Still, a reduction in enquiries doesn’t necessarily mean a reduction in business. As one independent bathroom retailer explained: “Whilst the latter stages of this year have seen less enquiries, we have reduced the amount of higher-mid offerings to more mid level to capture those with less budgets that perhaps feel that from the look of our showrooms, we are out of their reach.

With this one recent change and by pricing each bay in the windows, this means people are more likely to pop in and enquire.”

Even for the roughly two-in-five retailers who have seen reduced footfall at the end of 2025, most acknowledge that “the quality seems to be better and the values are higher”, as one kitchen and bathroom retailer thought.

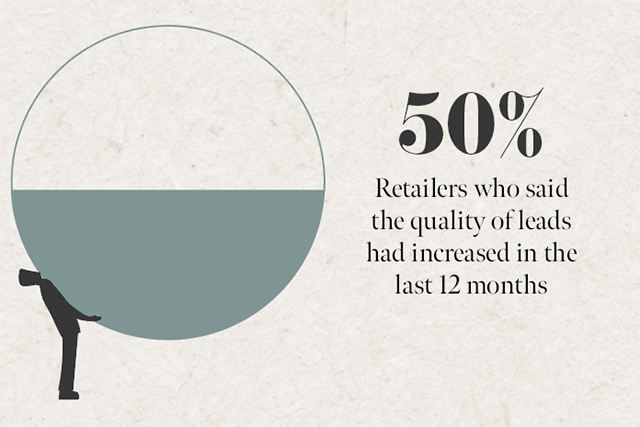

In fact, half of retailers said the quality of leads has increased a lot or at least a bit, with 30% saying they had stayed the same. However, when looking at the difference between kitchen and bathrooms, 63% of bathroom retailers saw lead quality increased versus 51% for kitchens.

As one bathroom retailer commented: “We’re seeing fewer people spending at the lower budgets, but those who are spending are investing more than they did last year.”

And although their lead quality hasn’t increased as much as bathroom retailers, one kitchen retailer said: “We have found that the customers are very switched on, and generally know what they want when we meet initially.

Often they will say they want a scheme that mirrors one on our website, which we are constantly updating with new projects. As these projects have increased in size and design, they want to emulate this and so the value naturally increases.”

And speaking of order values, 70% of retailers said theirs had gone up slightly or significantly, but many said that this was likely due to rising prices rather than clients’ willingness to invest more.

“We’ve seen increases in average order value for the last two years,” one kitchen retailer confirms. “However, some of this is to be expected due to price inflation in both product costs and labour costs.”

Meanwhile, a bathroom retailer estimates: “The cost of goods have increased on average 7-10%. The cost of installation has also increased, by approx 10% due to wage increases.”

In fact, as one kitchen retailer mused: “Once you factor in supplier price increases the order value is roughly the same as it was – our margins haven’t really changed.”

Conversion rates

A fifth of retailers (21%) said they had a conversion rate of less than 40%, nearly a third (31%) put it at 40-60% and 27% at 60-70%. Another 21% put their conversion rate at over 70%.

Although acknowledging that their conversion rate had slipped slightly, one retailer said: “I have pushed my prices up to increase margins. So we’re losing a few jobs that are more price sensitive but benefitting from improved profits on the jobs we do get.”

However, broadly speaking, most retailers anecdotally said their conversion rate was roughly the same year-on-year. “Our overall enquiry-to-sale conversion is broadly similar,” one kitchen retailer reported, “but the key figure for us is the conversion of qualified leads. Once a customer has received a design and quote, around 60% now go on to place an order.”

And as retailers lead such busy lives, and they already have enough on their plates to worry about anyway, a good few respondents confessed that they personally weren’t too worried about if their conversion rates were up or down at all.

As one candidly admitted: “Our conversion hasn’t changed and we acknowledge there is certainly room for improvement in this area of the business, but to be honest, we don’t know where to start with it!”

13% of retailers said the time between enquiry and confirmation was less than a month and nearly a third (30%) said it was between one and two months. There was a significant difference, however, between bathrooms and kitchens – a quarter of bathroom retailers said they convert in less than a month, compared to only 6% of kitchen retailers.

One bathroom retailer – who did say that their average time had remained about the same this year – exclaimed: “Clients want everything immediately! Generally they are coming to us much later in the refurbishment stage rather than pre-planning. Usually have the builder already started or starting in a week or two.”

However, on the total opposite end of the spectrum, one kitchen retailer observed that their project completion timings had actually slowed considerably over the past year. “We would normally look at it taking about a month,” they reflected. “But no one is keen to part with their money, even if they are committed.”

“Every year it gets longer,” agreed another kitchen retailer, who reports an average of two to three months between enquiry and confirmation, adding: “Though speaking to other retailers and suppliers, a lot is down to the projects we’re dealing with and so it’s a reflection of the market.”

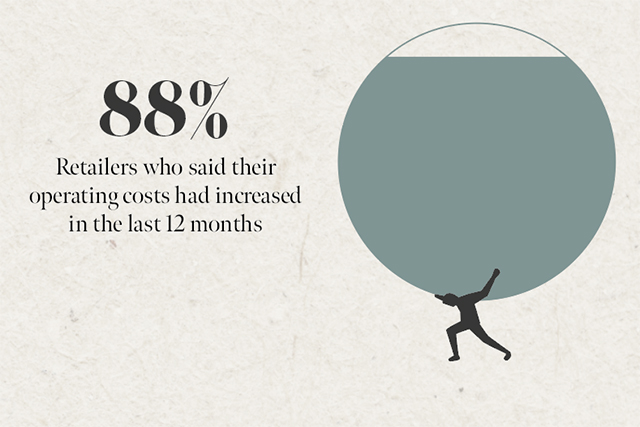

Operating costs

One thing virtually all retailers (88%) could agree on was that operating costs had increased in 2025, with 38% saying it had increased significantly.

“We’ve had business rates double (we have four premises so this is a big jump) and National Insurance has increased, let alone increases in some taxes also,” said one bathroom retailer, summing up an incredibly common response to this year’s survey.

“At times such as the VAT bill deadline, we’ve had some proper looking down the back of the sofa for cash moments,” said another, acknowledging that “cash flow has often been our biggest headache this year”.

Worryingly, one of the nearly two-in-five retailers who said their costs had increased significantly said: “Like everyone else, you look to what margin you really need to be working on, then you look at what you need to just survive…”

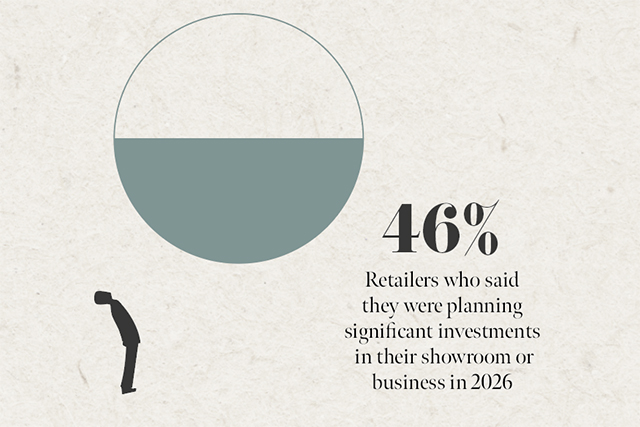

Showroom spending

But despite any uncertainty about the market, the confidence levels meant that 46% of retailers said they were planning significant investments in their showroom or business and another 14% hadn’t made their mind up yet. However, 47% of kitchen retailers said they had no plans compared to 29% of bathroom retailers.

By far, the most common showroom investment retailers mentioned was updating or even significantly increasing their number of displays. However, many business owners also said they planned to invest further into other areas of their showrooms as well, particularly to enhance the customer experience.

This spring, one bathroom retailer said they were planning a “partial refit will include an actual presentation room, an accessible working display, and a wellness suite”. Another bathroom business owner spoke about their plans for “a sitting coffee area for designers and architects, and a special space for samples and moodboards”.

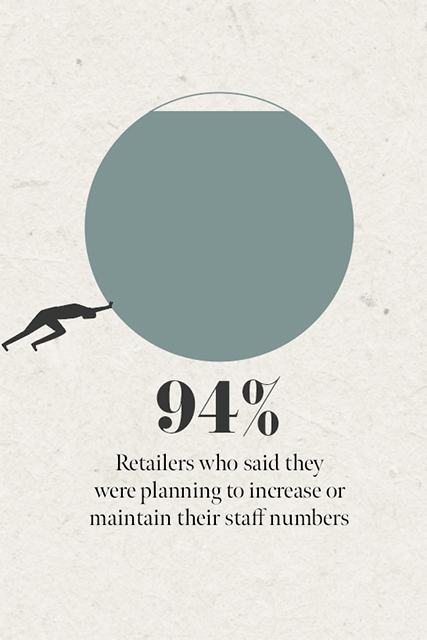

Aside from just investments into displays or showrooms, many retailers are also planning on investing in things like their marketing, business management software, vehicles and expanding their staff.

On that topic specifically, a quarter (24%) of retailers said they were planning on increasing the number of staff and 70% said they weren’t planning a reduction – a reassuring statement on the importance of good people in independent businesses.

Encouragingly, most of the retailers in this year’s survey said their staff expansion plans were either a result of planned growth this year, or even because enquiries have increased to the point that they need more hands on deck to meet the demand.

One independent retailer said they were looking to take on a new member of staff “to provide us with further opportunities to approach new business whilst maintaining our high levels of service,” adding, “If our business increases then we will also be looking to add another kitchen fitter to our already seven-strong installation team”.

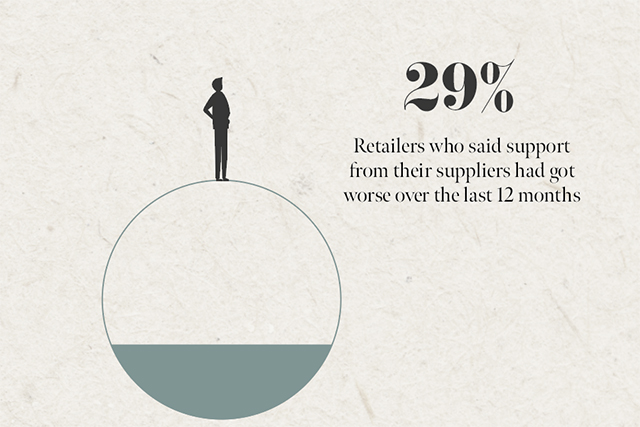

Supplier support

60% of retailers said that the support from suppliers was “good” or “excellent” with a third (32%) saying it was “average”, and that was pretty consistent across kitchen and bathrooms. However, 29% of retailers said support had got worse over the last 12 months – with 56% saying it was about the same, leaving just 15% saying it had got better.

When asked why, responses varied wildly, however most theorised that the number of actual sales reps employed by suppliers has dwindled in recent years. “We’ve seen significant changes in supplier personnel over the past couple of years,” one retailer explained, adding: “Many new representatives are not staying in post for long, resulting in limited relationships and long-term understanding. Too often, we’re met with inflexibility.”

Similarly, another who thinks support has slipped explained: “Being based in Cornwall, we naturally receive fewer visits, and there has been a noticeable turnover of reps in our area.

However, we have found that many companies are becoming stretched on the customer service side. There have been a couple of brands where we haven’t seen a rep since we opened.”

And on a related topic, we also asked retailers if they felt like suppliers understood their business and what they needed to do to make it profitable. A quarter of retailers said that suppliers’ understanding wasn’t great however 40% said it was good or excellent.

Anecdotally, most retailers felt like supplier understanding was a mixed bag, and while some were leaps and bounds ahead, others are sorely lacking. As one retailer said: “The support we get from some of our suppliers is excellent. They go above and beyond, they are interested in our business, want to build positive relationships and have been a great support for training.

“But for some – and this is a generalisation of the weakest – they have just dropped off completely and you can see it’s a part of their culture within their business/corporation. It’s essentially a lack of aftercare and poor representation.”

“Some are good, and some bad,” one independent bathroom retailer concluded. “Over time, you start to support the good and forget the bad.”