The 2025 Kitchen Market Report

After another tough year for kitchen sales and installation, the latest JKMR 'Overview Report on the UK Fitted Kitchen Market' reveals a surprisingly resilient picture of the industry – with independent studios leading the charge in value growth. Jayne Barber digs into the data and what it means for the road ahead…

Words: Jayne Barber

Our latest report into the UK fitted kitchen market paints a picture of an industry still finding its feet after a turbulent few years. While headlines around falling installation numbers continue to dominate, the deeper analysis shows a more complex – and, in some areas, surprisingly resilient – reality.

Let’s start with the figures. In 2024, the total number of new kitchen installations slipped once again, with completions falling to just under 1.05 million, a drop of more than 18% on 2022 levels.

That marks over two years of household caution when it comes to major discretionary home refurbishments, a trend reinforced by reduced new build housing completions.

But, despite lower volumes, market value has held up. In fact, it’s risen.

In 2024, fitted kitchen product sales – covering cabinetry, worktops, integrated MDAs, sinks and taps – reached almost £5.4 billion at end-client buying price. That’s a 3% increase on 2022. With volumes down, this means average spend per project was nearly 22% higher.

This rise in per-project value has been driven by improved product specification across the board, and a noticeable shift toward larger kitchens. That said, it would be wrong to interpret this as a clear signal of growing profitability. Business and staff costs have risen sharply across the industry, making margin growth a challenge for many players.

And this is where the story diverges between market sectors.

It’s important to stress that the kitchen market is not homogenous. What holds true for one sector may not apply across the board.

Take the overall rise in market value: while the total grew by 3% from 2022 to 2024, income from fitted kitchen products in the specialist studio sector rose by more than 9% in that time. That’s a strong performance, especially when set against the relative flatlining of other segments.

For example, income from Howdens, when looking specifically at kitchens installed into family dwellings (as JKMR defines this market), was essentially unchanged from 2022. Meanwhile, for most other mass volume multiples, income was at least 8% down – in some cases more.

Even the Direct Contract sector, which supplies new build and housing associations directly at factory gate pricing, proved more resilient than might be expected, considering the drop in housing completions. Income here was down by just 6% from 2022, supported in part by the rising proportion of higher-end family homes within the new build mix.

Why specialists are standing firm

The studio sector has, in relative terms, performed strongest over the last two years. Clients operating at the higher end of the budget spectrum have shown themselves to be more financially resilient and more willing to invest meaningfully in a new kitchen.

As a result, the studio channel has regained an almost 40% share of total market value. While that hasn’t translated into notable gains in installation share, it does underline the enduring value and importance of this part of the market.

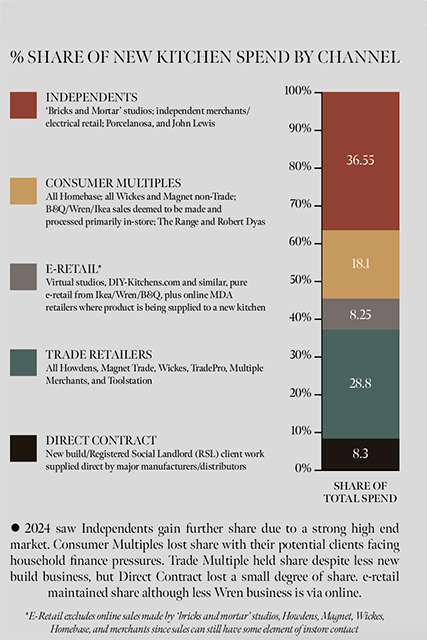

Over the past decade, the trade supply route has grown dramatically in importance – particularly in the owner-occupier refurbishment market. Today, it sits almost on par with consumer-facing channels in terms of volume.

In 2024, kitchens for the owner-occupier refurb market were supplied in nearly equal numbers via trade-facing operations (including Howdens, trade terms at Wickes and B&Q, MKM, Huws Gray etc.) and consumer-facing businesses (such as studios, Wren, DIY-Kitchens.com, and non-trade sales from the sheds).

But in value terms, there’s still a clear divide. The consumer-facing sector invoiced almost £3 billion worth of products, compared to just over £1.1 billion from the trade-facing side.

That reflects the significant price differential between studios and trade accounts. However, it’s worth noting that what a tradesperson pays for their kitchen from a Howdens or MKM isn’t necessarily what the end consumer sees on their invoice.

From the householder’s perspective, the perceived value – and cost – of a trade-supplied kitchen may not be markedly lower than one bought directly from a studio or consumer brand.

Looking ahead

At JKMR, we do not expect 2025 to bring a dramatic uplift in kitchen installation numbers. While the market is showing signs of price-led value growth – thanks in part to rising business costs – wider consumer sentiment remains cautious. Concerns over house prices, potential tax increases, and the general economic climate continue to suppress confidence.

Meanwhile, despite government rhetoric, we do not anticipate a substantial rise in new-build completions. The private rental refurb market also remains constrained by ongoing structural challenges.

That said, by 2026 we expect the picture to start improving. A new kitchen will continue to be seen by many as a sound investment – both practically and emotionally. As the central space in the modern home, the kitchen is now the family hub and the property’s social centrepiece.

We believe both the new build and owner-occupier refurb sectors will begin to grow again, albeit modestly. We also expect continued changes in how – and where – consumers choose to buy.

Changing retail dynamics

When the kitchen market recovers from a downturn, it’s common to see changes in the retail landscape. We’ve seen it before and there are signs we may be seeing it again.

Notably, several mass-volume players, including Wren, are actively exploring the idea of smaller-format, high street showrooms. If fully realised, this could flip the traditional model on its head with mass market retailers targeting prime town-centre footfall, while many independent studios continue to operate from more cost-effective, edge-of-town locations with free parking.

How such a shift might affect the pricing strategies of volume players remains uncertain. But it could have implications for the growth of studio franchises and buying groups, offering independents access to national-level support structures, shared marketing, and advertising resources.

Key questions

Looking further out, there are still many unanswered questions.

How will AI and online planning tools reshape the buying journey? What does the rise of remote consultations and digitally confident consumers mean for showroom footfall? Will challenges to Howdens emerge in the trade space? Can the Homebase name help The Range evolve into a credible kitchen destination? And what do the next generation of kitchen buyers really want?

None of these questions have easy answers but each has the potential to impact both the structure and the scale of the market.

At JKMR, our view is cautiously optimistic. The market remains in a period of recalibration, but the fundamentals, especially in terms of consumer aspirations for the kitchen space, are still strong. For those willing to evolve with the market, the coming years offer not just challenges, but real opportunities.